As if the housing market slowdown were not enough to challenge local contractors, now Holmes Beach City has stopped issuing all building permits.

The City of Holmes Beach Commissioners decided the building department stop granting “requests for construction, reconstruction, or improvement of buildings or structures within the flood hazard areas” beginning February 12th. All building is halted while compliance is being studied and codes compared with other communities.

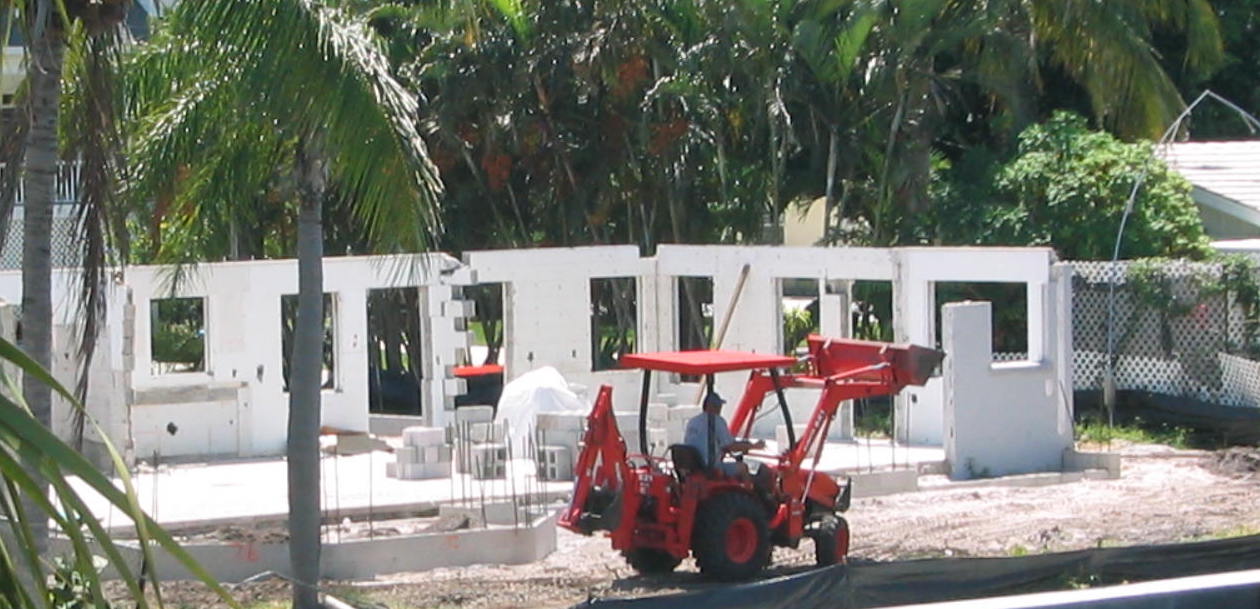

Caught in this moratorium is a partly rebuilt 1950’s house. New walls, windows, and roof were constructed last month but work has now stopped. The city is considering that it may even have to be torn down again.

Most people who have gone through a house remodel or renovation project know that some construction requires applying for a city permit and subsequent approval by the city building inspector. Zoning and building codes mandate what a property owner can construct and to what standard.

Zoning regulations usually come from local agreement on what type of community people desire. But building codes are governed by national, state, and local rules that evolve over the years, some for safety, and some for consistency.

We probably all agree that electrical and plumbing codes are for our safety and health. What about structural codes? It would be prudent to build a house that stands up to the elements: weatherproof, wind resistant, fire resistant, naturally lit, ventilated, and efficiently warmed or cooled. Architectural and engineering challenges to these requirements have occupied minds for thousands of years.

So what are some building solutions to the elements when you live on a low-lying, barrier island in a hurricane zone? Historically, indigenous tribes chose to live on the protected mainland and make fishing excursions to the island for food. Over the last century modest vacation houses appeared on the beach and waterfront. Infrequently a hurricane blew down structures and flooded the island. People rebuilt. The incidence of destructive hurricanes was low for much of latter 20th century, the risk of loss seemed minimal, and the cost of rebuilding acceptable. Insurance was seldom considered necessary or even obtainable.

Without going into the origins of the Federal Emergency Management Agency, well-intentioned legislators created a plan in 1968 to insure people’s houses from flood loss by transferring the cost to taxpayers. Banks loved this idea and required mortgaged houses in flood zones to have flood insurance. Private insurance companies loved it because it removed their risk to flood and they stopped including coverage.

As demand for waterfront living exploded and the risk of loss was covered by cheap government insurance, building boomed. As potential and claimed insured losses skyrocketed, some rules changed in 1976. The FEMA run National Flood Insurance Program used weather data to determine ‘100 year’ flood plain levels and priced policies according to building design in that flood plain.

Most of Anna Maria Island is around 4 to 6 feet above sea level. A once in 100-year flood event is considered to raise water to 9 feet (11 feet in some parts). A Category 5 hurricane could create a surge of 25 feet above normal sea level.

New construction has to have living space above the flood plain, which meant the first floor has to be elevated above 9 feet. Houses built before 1976 can remain but new work must comply with the new code. Owners are exempted if their old structure’s remodel is less than half the house value. This exemption is commonly referred to as ‘the 50% rule’.

You can put in a new kitchen, bathroom, even add a bedroom, and retain your ground floor living if the numbers work. That’s why some old cottages remain, some are remodeled, some are razed, and all new houses are built elevated. It’s easy to spot a pre-1976 house, even if extensively modernized, because it has ground floor living space.

Of course most people prefer to live on the ground floor with easy access to patio, pool, boat, and cars. That puts preferences in direct conflict with the government’s desire to protect people from their own choices. Also, desire for larger area homes squeezed living space between the flood plain and the 37ft height restriction. The result was that most new construction was built 3 stories high and lot-line to lot-line.

However, increasing appraised values raised the 50% remodel figure. Obsolete plumbing, wiring, or termite damage could be excluded from the improvements valuation. And slower real estate activity brought down the price contractors charged. There is some confusion in how many and how frequently you can do a ‘minor’ remodel. The house pictured was approved for remodeling and the plans apparently complied with the 50% rule. So why did the Holmes Beach Commissioners question the building department permits?

All the above is related to FEMA flood insurance compliance only. Wind, fire, and theft insurance is provided by private companies. The Florida building code dictates how a house is constructed for safety and health, but the government also dictates how you live in that house. It is saying literally that you can’t have a bedroom in the flood plain.

If you borrow money for your home purchase the mortgagor may require all hazards insurance, but you can only get flood insurance from FEMA NFIP. If you own your home outright you could forgo buying insurance, i.e. self-insure, which is what a lot of people do, considering the high cost of wind damage coverage, and you can decide not to buy flood insurance.

According to the government, what you can’t do is build and live on the ground floor in the flood plain. But what are they trying to protect people from? If you choose to buy, build or live in an area that gets 15 to 25 hurricanes per year, would your biggest worry be a flood while you’re asleep? Even if your house is built above the flood plain would you not evacuate from an approaching hurricane? (Apparently not if you lived in New Orleans!) Do we need the government to enforce common sense and should we all pay for its mandates even if they are well-intentioned?

As we have seen from the tragic losses of Hurricane Katrina, FEMA could not get people out of harm’s way and they are incompetent in the aftermath. What is it we are paying for, again?

7 replies on “We’re Here To Help You”

Update March 18th:

Holmes Beach City Commissioners met last week and decided they needed to speed up the process of changing the building codes to meet FEMA floodplain regulations. To ‘fast-track’ the changes, they want to reduce the delay by having one hearing and reading instead of two. The building permit moratorium has put many contractors on hold and out of work. Mayor Bohnenberger thought another four weeks could see a new ordinance ready for discussion.

[…] 31-page ordinance is the result of FEMA, (We’re Here To Help You), having questions about code implementation and compliance with current […]

Update April 2nd:

New ordinance first reading

[…] months ago the City of Holmes Beach reviewed its building code after discussion with FEMA rules on floodplain […]

“Obsolete plumbing, wiring, or termite damage could be excluded from the improvements valuation”

I have an older FL bungalow that we are in love with, we happen to be located in flood zone A.

We have all three issues quoted above, obsolete plumbing, wiring and termite damage, that we would like to repair in our home. I have searched FEMA and can not find anywhere that states those exclusions.

Can some one please help in directing us to a FEMA document that lists the above exclusion. Our local building department here is stating that all those items must be included in the 50% remodel rule, that would force us to demolish the house or spend $75K to raise it.

Thank you in advance for your help

Rod

In love with Old Fl!

Rod,

I don’t know if the answer is in the FEMA documents, but I do think that the regulations have been interpreted differently by each local building department.

I suspect that the Feds have clamped down on some arbitrary exclusions that the building department previously allowed.

Another gray area is how frequently the 50% remodel can be applied. If you have time, upgrades might be permitted in succession.

Good luck and thanks for your comment.

“Another gray area is how frequently the 50% remodel can be applied. If you have time, upgrades might be permitted in succession.”

Mike,

Thank you for your prompt reply.

Yes we were hoping to take our time and do the remodels over the course of a few years; our county allows reassessment once a year from permit date. Unfortunately our local city building department has adopted a more strict approach and counts the updates cumulatively. So the new 8k roof we put on the house last year still counts towards our 50% depreciated building value.

We were advised that we could have the building reassessed and increase the 50% value.

Have contacted a few local appraisers and they have no interest in opposing the county. Stating that the county is very strict on there evaluations and question them if they increase the value at all.

Looks like another battle will be lost to progress. One of the reasons FL seems to have no history at all. They only value the shiny and new.

Rod

In love with Old Fl!